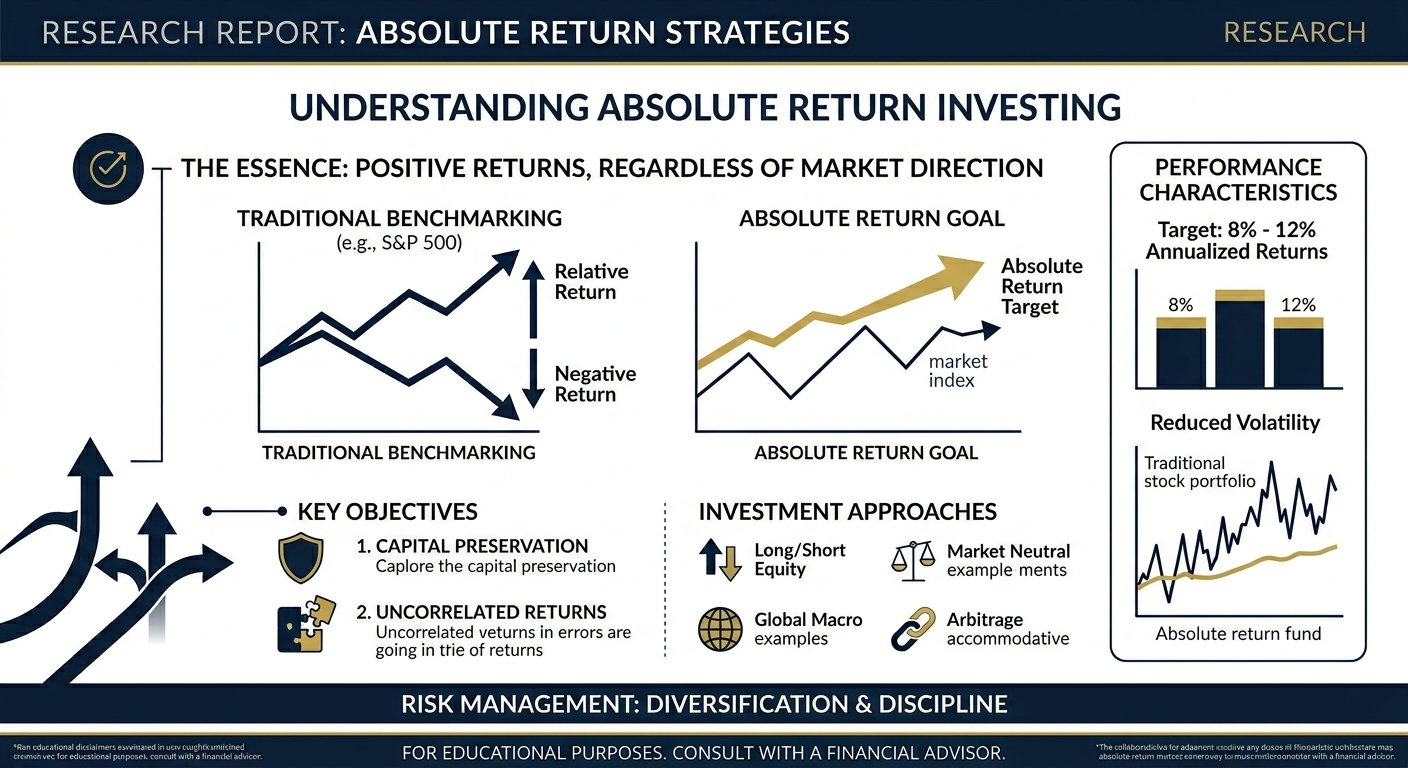

Most investors are familiar with one basic idea: buy a diversified portfolio, hold it for the long term, and hope markets go up. This approach — often called relative return investing — measures success by comparing your returns to a benchmark like the S&P/TSX Composite or the S&P 500. If the index falls 20% and your portfolio falls 15%, that's considered a good year.

Absolute return investing starts from a different premise. The goal is not to beat a benchmark. The goal is to make money — in actual dollars — regardless of what markets do.

This distinction matters more than most people realize, especially for investors who cannot afford to sit through a prolonged drawdown and wait for recovery.

Relative Return vs. Absolute Return

In a traditional portfolio, your returns are tied to market direction. When equities rise, you make money. When they fall, you lose money — and you measure success by how much less you lost compared to the index.

Absolute return strategies reject this framework. Instead of asking "did we outperform the benchmark?", the question becomes "did we generate a positive return, and did we protect capital when markets declined?"

This is not just a philosophical difference. It changes how portfolios are built, how risk is managed, and what tools are used.

A relative return manager might stay fully invested in equities at all times, because being out of the market risks underperforming the benchmark. An absolute return manager has no such constraint. They can hold cash, hedge exposures, go short, or shift between asset classes based on where they see the best risk-adjusted opportunities.

How Absolute Return Strategies Work in Practice

There is no single absolute return strategy. The term covers a wide range of approaches, but most share a few common characteristics:

Active position management. Unlike passive or index-tracking strategies, absolute return managers actively decide what to own, what to short, and how much risk to take at any given time. Positions are not static — they change as market conditions evolve.

Use of hedging. Most absolute return strategies use some form of hedging to reduce exposure to broad market moves. This can include short selling individual securities, using options, or taking offsetting positions in futures markets. The intent is to generate returns from specific investment ideas rather than from overall market direction.

Focus on risk control. In relative return investing, risk is often defined as deviation from a benchmark. In absolute return investing, risk means losing money. This leads to a much more direct approach to risk management: strict position limits, defined stop-losses, and active monitoring of portfolio drawdowns.

Diversification across sources of return. Many absolute return managers invest across multiple asset classes — equities, fixed income, currencies, commodities — and use multiple strategies within a single portfolio. The logic is that if one strategy underperforms, others may offset the loss.

Common Types of Absolute Return Strategies

Long/Short Equity. The manager buys stocks expected to rise and sells short stocks expected to fall. The combination of long and short positions reduces net market exposure, meaning the portfolio is less sensitive to broad market swings. Returns come from the manager's ability to pick winners and avoid losers, not from the market going up.

Global Macro. These strategies take positions based on macroeconomic themes — interest rate changes, currency movements, trade policy shifts, commodity cycles. Positions are typically expressed through futures, options, and foreign exchange markets rather than individual stocks.

Quantitative / Systematic. Rule-based strategies that use mathematical models to identify patterns and execute trades. These can range from trend-following systems in futures markets to statistical arbitrage in equities. The key advantage is discipline — the model follows rules without emotional interference.

Multi-Strategy. A combination of the above, managed within a single portfolio. The goal is to generate returns from multiple uncorrelated sources, reducing reliance on any single strategy or market environment.

Who Should Consider Absolute Return Investing?

Absolute return strategies are not for everyone. They tend to be most appropriate for investors who:

Cannot tolerate large drawdowns. If you are retired, managing a foundation, or simply cannot afford to lose 30-40% of your portfolio in a market downturn, absolute return strategies offer a different risk profile than traditional equity portfolios.

Want returns that are less correlated to stock markets. Many institutional investors — pension funds, endowments, family offices — allocate to absolute return strategies specifically because the returns behave differently from their existing equity and bond holdings. This improves overall portfolio diversification.

Have a long enough time horizon to evaluate the strategy properly. Absolute return strategies may underperform a rising stock market in a strong bull year. Their value shows up over a full market cycle, including periods of decline. Evaluating an absolute return manager after one year of a bull market is not a meaningful test.

Qualify as accredited investors. In Canada, most absolute return strategies are offered through exempt market products — pooled funds or separately managed accounts — that require investors to meet accredited investor thresholds. This generally means annual income over $200,000 (or $300,000 combined with a spouse) or financial assets exceeding $1 million.

What Absolute Return Investing Is Not

It is worth clarifying a few common misconceptions.

It is not risk-free. Absolute return does not mean guaranteed positive returns. It means the manager's objective is to generate positive returns in all environments, but that objective is not always achieved. Losses can and do occur. The difference is that risk management is central to the process, and protecting capital is an explicit priority.

It is not market timing. Absolute return managers do not simply try to predict whether markets will go up or down. Most strategies involve taking specific positions based on research and analysis, hedging unwanted risks, and managing exposure dynamically. This is different from making binary bets on market direction.

It is not just for institutions. While absolute return strategies have traditionally been associated with large institutional investors, they are increasingly accessible to qualified individual investors through pooled fund structures and separately managed accounts.

Canada's investment landscape

Canada's investment landscape has historically been dominated by long-only equity and bond strategies, with heavy home-country bias toward Canadian banks, resource companies, and real estate. This concentration served investors well during certain periods, but also created significant vulnerability during downturns — particularly in 2008, 2015 (energy sector), and 2020.

A growing number of Canadian investors are recognizing the value of strategies that do not depend on these same market exposures. The Canadian hedge fund industry, while smaller than its U.S. counterpart, has been expanding steadily, with firms in Vancouver, Toronto, Montreal, and Calgary offering absolute return mandates across equities, currencies, commodities, and fixed income.

For investors seeking to diversify beyond traditional Canadian portfolio construction, absolute return strategies represent a fundamentally different approach to managing capital — one where the first question is not "what is the benchmark doing?" but "are we protecting and growing our clients' money?"

How YL Capital Approaches Absolute Return

At YL Capital, absolute return is not just a label — it defines how we build and manage portfolios. Our strategies combine fundamental research, quantitative models, and active risk management across equities, currencies, and commodities. We size every position with a defined risk budget, and we hedge portfolio exposure when market conditions warrant it.

Our objective is straightforward: generate positive returns over time while keeping drawdowns within strict limits. We believe this approach serves investors who want their capital actively managed — not passively exposed to market cycles.

YL Capital is an independent investment management firm based in Vancouver, Canada. For more information about our absolute return strategies, visit oursite or contact us.

Views expressed are those of the author as of the date of publication and do not constitute investment advice. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal.